The new capital rules for banks will have noticeable consequences for many companies. Surety bonds and other alternative financing tools are becoming more attractive.

Basel IV, which took effect at the beginning of 2025, further tightens regulatory capital requirements for banks. This will affect both lending volumes and loan terms. To put this in context: a central element of the new framework is the so-called output floor, which limits the benefits of internal bank models. Until now, the internal risk models used by many banks have typically produced lower capital requirements – and thus lower risk-weighted assets (RWA) – than the standardized approach. Under the output floor, however, banks must also calculate RWA using the standardized approach, and their internally calculated RWA must be at least 50% of the RWA under the standardized approach. By 2030, the output floor will rise to 72.5%.

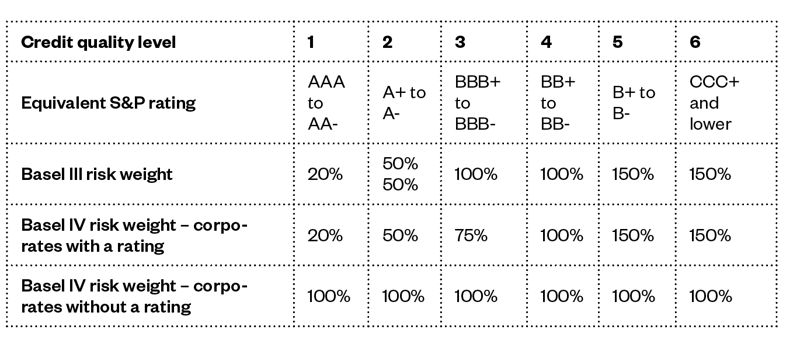

Depending on a company’s credit quality, the impact will differ. The following overview summarizes the changes:

Financing challenges are intensifying

In practice, this tightening is likely to force banks to hold more capital and to increase their risk-management operating costs. Institutions that have relied heavily on internal risk models and have therefore benefited from lower capital requirements than under the standardized approach are particularly likely to tighten their lending terms.

In plain language: bank loans – and bank guarantees such as letters of credit – are likely to become more expensive, and companies may find it harder to obtain or renew financing. This development could further exacerbate the situation in sectors that are already facing major challenges. This is not about isolated cases: according to German Creditreform, nearly three quarters of companies in the automotive industry had no external rating as of mid-2024.

Act now

Companies that have relied heavily on bank financing should step up communication with their lenders, increase the transparency of their financial reporting and diversify their funding sources – for example through factoring, private debt or surety bonds. As Basel IV takes hold, banks are likely to scale back their guarantee lines even further. Surety providers stand to benefit from this trend, as Basel IV does not apply to them.

For you as an insurance broker, it might be helpful to tap into gracher’s 360° financing advisory capabilities for your corporate clients. We can present attractive alternative financing options, identifying the most competitive market terms. In addition, we can structure solutions that combine multiple instruments and financing partners. Syndicated facilities have the advantage that each individual lender reduces its exposure, while larger facilities – that a single lender might have declined – can still be financed.

Talk to us about how Basel IV could affect your corporate clients and what steps to take next. Find out more at www.gracher.de